Two reports about the state of the banking system came out this week:

- OCC’s Semiannual Risk Perspective Highlights Key Risks in Federal Banking System – Semiannual Risk Perspective Spring 2026

- Federal Reserve Board’s Financial Stability Report – Financial Stability Report, May 2026

Certain findings in the two reports point to the need for a bank to develop stress scenarios beyond the DFAST regulatory scenarios to explore emerging risks, and to keep those scenarios current as uncertainty rises.

Thus, in its report OCC highlighted credit, market, operational, and compliance risks, as key risk themes in its report. For credit risk in particular, credit conditions and refinancing risk in certain segments of commercial real estate (CRE) lending and of private credit markets warrant ongoing monitoring.

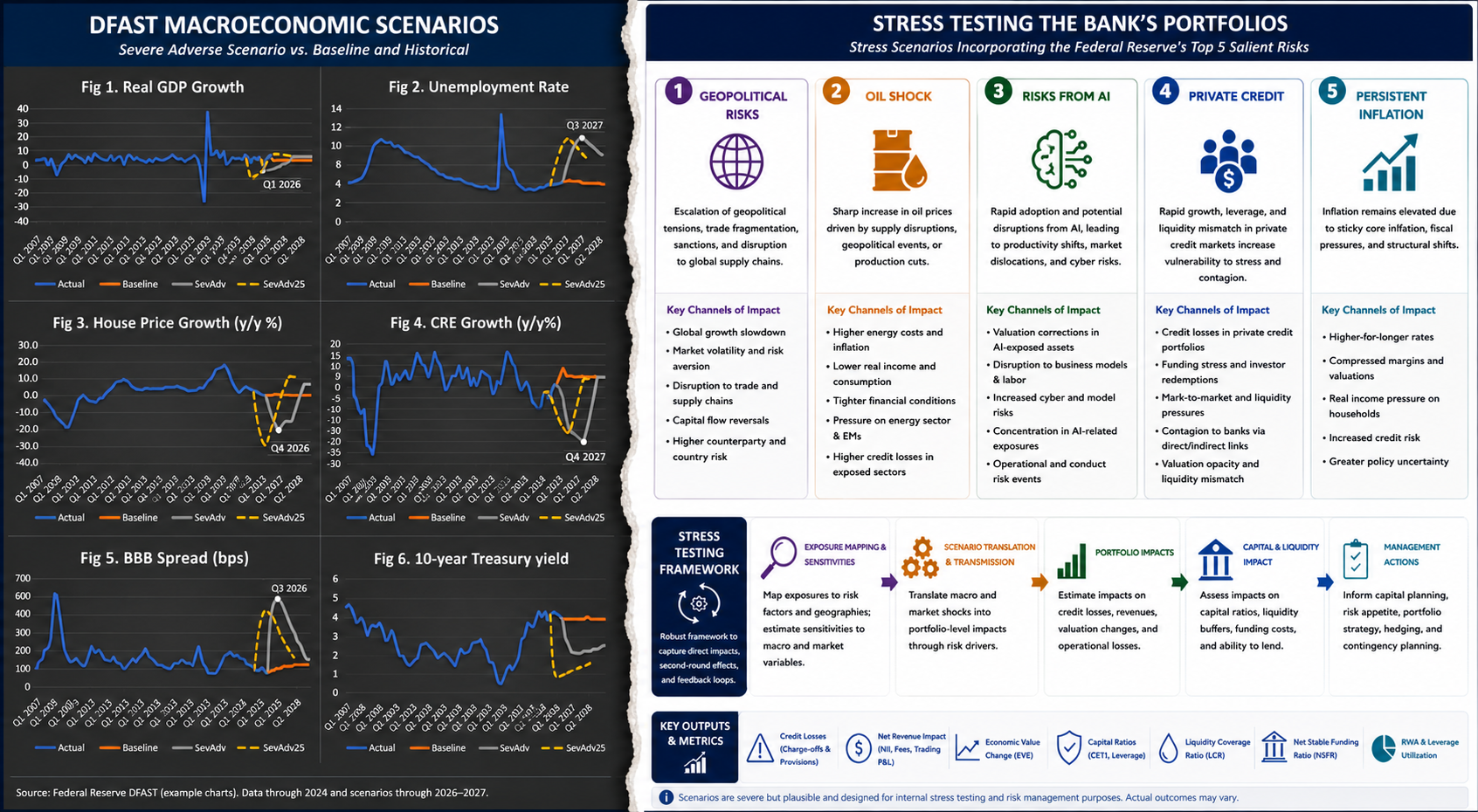

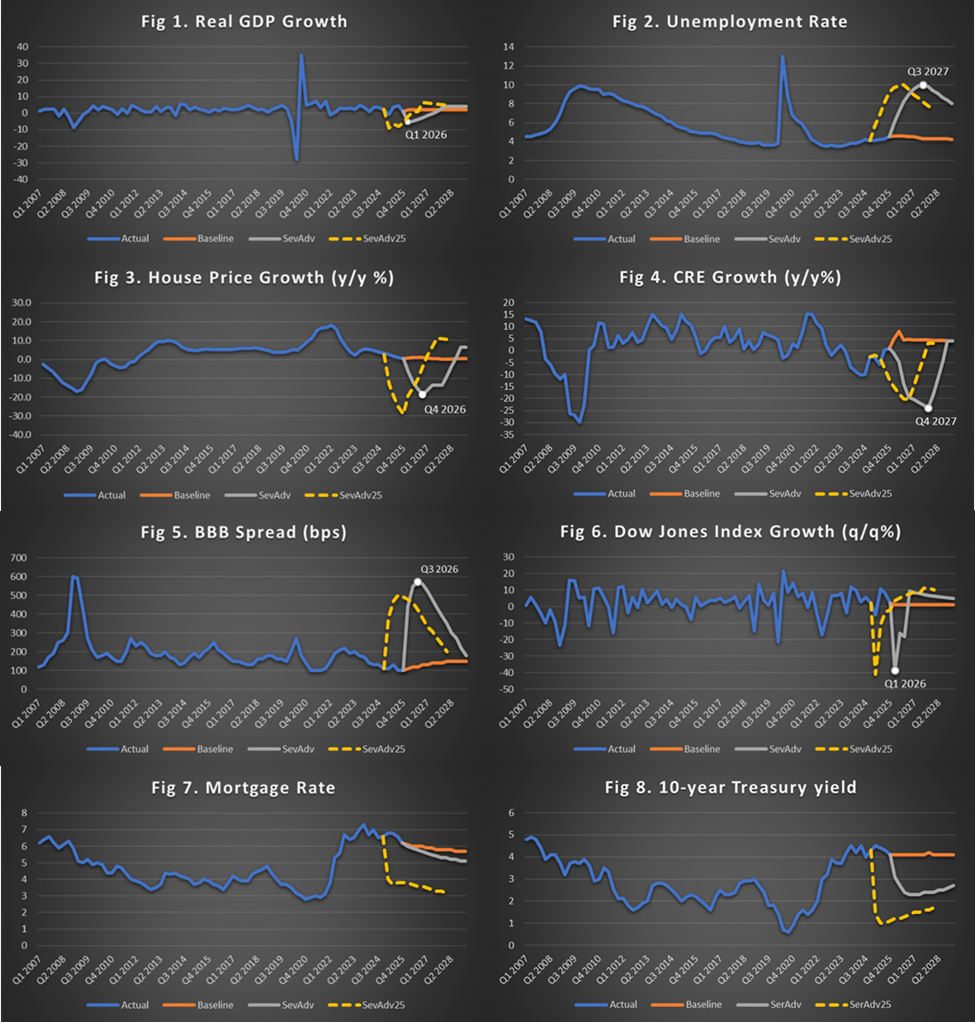

The DFAST 2026 stress tests scenarios released by the Federal Reserve in February include baseline and severely adverse scenarios for CRE prices. They are depicted in Figure 4 of the chart collage below.

Reflecting the above concerns, the 2026 severely adverse scenario for CRE y/y price growth reaches a lower trough than the respective 2025 scenario, -24% vs. -20.5%. This compares with the trough of -30% reached in Q4 2009.

In fact, amongst the eight macroeconomic factors shown in the chart collage below, CRE price growth and BBB Spread are the only ones whose 2026 severely adverse scenario have a worse trough (or peak) than the respective 2025 one. This indicates that the DFAST 2026 severely adverse scenario would lead to similar or milder loss forecasts compared to the ones reported from the 2025 exercise, except for the banks with significant CRE and/or C&I exposure.

On the other hand, the DFAST 2026 scenarios do not include a scenario for private credit.

OCC’s report states that bank exposures to private credit funds are generally performing according to the terms agreed with borrowers. There are signs that credit quality for some vintages, borrower types, and sectors of the private credit markets is weakening. The increasing use of debt restructurings and paid-in-kind (PIK) mechanisms may mask underlying credit deterioration in loan portfolios held by private credit funds[1]. In conjunction with growth in lending to private credit funds and an increase in concentrations at some banks, careful monitoring of borrower performance and refinancing risk is increasingly important.

US banks’ lending to Non-Depository Financial Institutions (NDFIs)—such as private equity funds and private credit firms—has experienced massive growth, with NDFI exposure hitting over $1.4 trillion by late 2025. Nearly 40% of Q4 2025 loan growth came from NDFI loans, which increased over $106 billion (7.3%) in that quarter alone. Loans to NDFIs now account for over 10% of total U.S. bank loans. In addition, banks have increasingly shifted from direct loans to providing credit lines to NDFIs introducing risks of sudden liquidity drains if these lines are drawn simultaneously during a crisis.

While large banks (GSIBs) hold ~87% of total NDFI loans, smaller regional banks are more exposed relative to their equity, with NDFI capital concentration rising to 6.3% for banks under $10 billion, compared to 1% in 2010.

Hence, the above point to the need for banks to develop and run a severely adverse scenario for NDFI lending in conjunction with a moderate U.S. recession that should account for contagion effects through fire-sale of assets. An example of such scenario consists of a rapid repricing of credit risk triggered by a U.S. recession and inflation persistence leading to sharp losses across leveraged NDFIs. Liquidity mismatches, margin calls, redemption pressure, and forced deleveraging amplify the shock. Banks experience stress through counterparty exposure, warehouse financing, subscription lines, prime brokerage losses, leveraged loan drawdowns, derivative exposure, and market-making inventories.

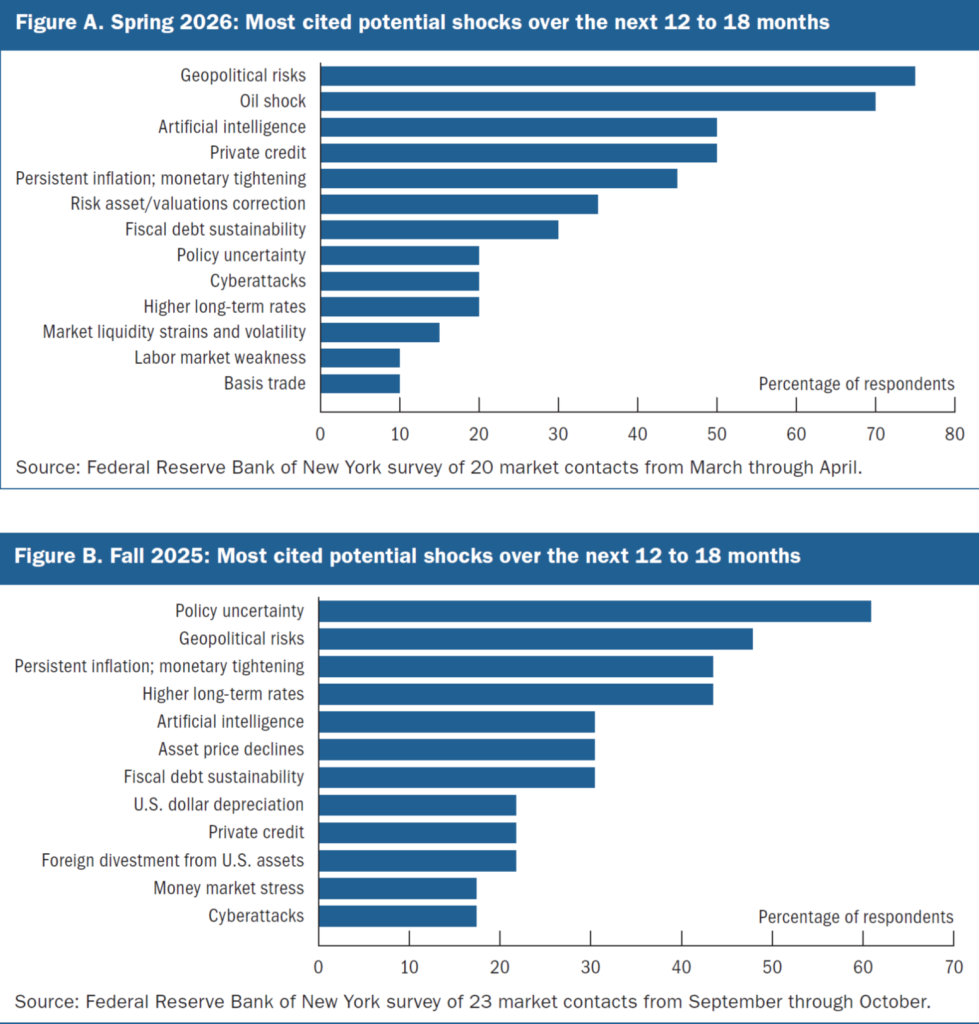

In its report the Federal Reserve refers to the Survey of Salient Risks to Financial Stability. It is a survey conducted by the Federal Reserve Bank of New York surveying 20 professionals at broker-dealers, banks, investment funds, and advisory firms. Figures A and B list the most salient risks in Spring 2026 and Fall 2025 respectively.

The top 5 risks are geopolitical risks, an oil shock, risks from artificial intelligence (AI), private credit, and persistent inflation. It is worth noting that geopolitical risks, risks from AI and persistent inflation were also amongst the top 5 risks in Fall 2025.

What would happen to your bank’s portfolios if a further increase in term premiums leading to higher-than anticipated long-term interest rates, particularly if accompanied by persistent inflation, could pose risks for both borrowers and lenders?

Concluding Remarks

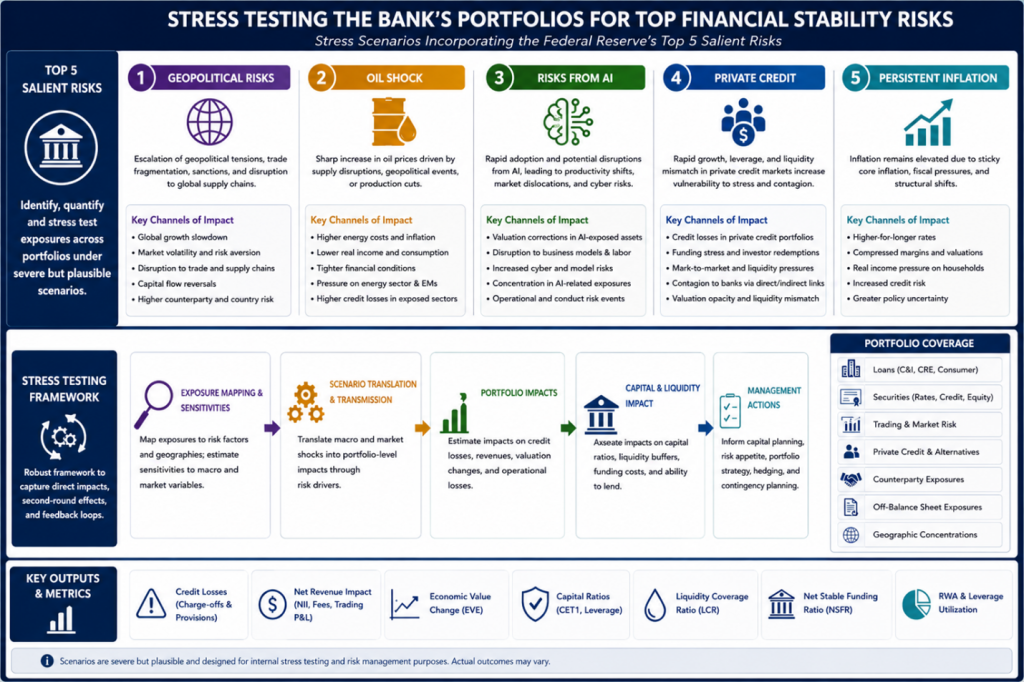

The above analysis of the two reports by OCC and the Federal Reserve underlines the importance for a bank to regularly update its own stress scenarios beyond the regulatory scenarios in order to explore emerging risks such as geopolitical risks, an oil shock, risks from artificial intelligence (AI), private credit, and persistent inflation.

In terms of credit risk, the DFAST 2026 severely adverse scenario would lead to similar or milder loss forecasts compared to the ones reported from the 2025 exercise, except for the banks with significant CRE exposure. This is because amongst the eight macroeconomic factors examined, CRE price growth is the only one whose 2026 severely adverse scenario has a worse trough (or peak) than the respective 2025 one.

Of course, the stress in the CRE price index is an average across CRE asset classes. However, the noncurrent ratio for CRE continues being driven by Office and Multifamily. What happens if a bank, for example, has higher concentration in CRE Office and Multifamily? In such cases, as previously argued[2], a bank should use scenarios for more granular CRE indices by asset class and geography for better accuracy in its loss forecasts and impact on capital. Of course, such granular scenarios should be conditional on the DFAST severely adverse scenario of the aggregate CRE index for consistency.

Similarly, what if a bank has significant exposures in manufacturing, oil & gas or agriculture? How would these industries be affected under a scenario of higher-than anticipated long-term interest rates, combined with persistent inflation and geopolitical risks?

Whether for loan level (bottom-up) or portfolio/bank level (top-down) stress testing, banks need relevant scenarios according to their geographical footprint and balance sheet mix. Such scenarios would enable a bank to stress beyond just credit risk for integrated stress testing as the chart below illustrates. Thus, within the integrated stress testing framework, the narrative of a scenario and its shocks are first run through the economic scenario generator to produce a multifactor economic scenario that is relevant to the geography and portfolios of the bank. The scenario is then applied by the framework engine to measure the capital and liquidity impacts for integrated bottom-up or top-down stress testing. This is the general approach we follow for our clients but customized to their balance sheet composition and geography.

References

[1] See also previous post on LinkedIn: https://www.linkedin.com/posts/grigoris-karakoulas-94209b71_private-credits-rising-pile-of-bad-pik-activity-7391507804789911552-IIzC?utm_source=share&utm_medium=member_desktop&rcm=ACoAAA8j-IIBzdPXC5k7XkbDp5yUjy8P-fU9hbU

[2] Karakoulas G., How Company-Run and Fed DFAST Projections Measure Up. RMA Journal, October 2023, pp.15-18; 2023 Stress Testing Scenarios | InfoAgora

Grigoris Karakoulas is a visionary business leader combining over 28 years of risk management and predictive modeling experience. He is the president and founder of InfoAgora (infoagora.com) which provides risk management consulting, predictive (AI/ML) risk analytics, deposit/credit price optimization, economic scenario generation, integrated stress testing/CECL, and model validation services. He is also Adjunct Professor in the Department of Computer Science at the University of Toronto. Grigoris has published over 40 papers on predictive modeling and risk management. He is on the PRMIA subject matter boards for Stress Testing and Enterprise Risk Management. He holds a PhD in Computer Science (Artificial Intelligence).

E-mail: grigoris@infoagora.com; Phone: (646) 380-1883.